In general, instead of arbitrarily choosing \(\lambda = 4\), it would be better to

use cross-validation to choose the tuning parameter \(\lambda\). We can do this using

the built-in cross-validation function, cv.glmnet(). By default, the function

performs ten-fold cross-validation, though this can be changed using the

argument folds. Note that we set a random seed first so our results will be

reproducible, since the choice of the cross-validation folds is random.

> set.seed(1)

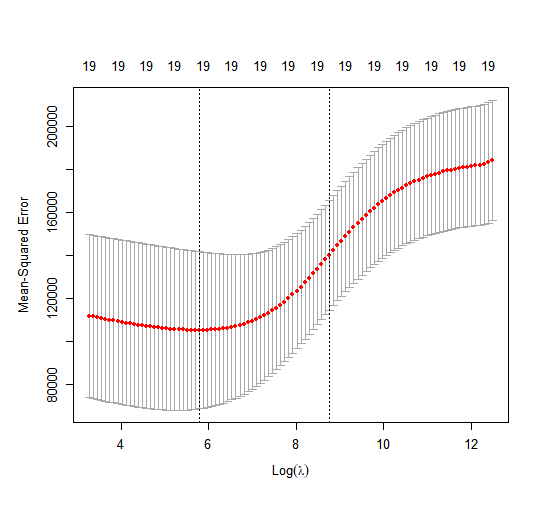

> cv.out <- cv.glmnet(x[train,], y[train], alpha = 0)

> plot(cv.out)

> bestlam <- cv.out$lambda.min

> bestlam

[1] 326.0828

Therefore, we see that the value of \(\lambda\) that results in the smallest cross-validation error is 326. What is the test \(MSE\) associated with this value of \(\lambda\)?

> ridge.pred <- predict(ridge.mod, s = bestlam, newx = x[test,])

> mean((ridge.pred - y.test)^2)

[1] 139856.6

This represents a further improvement over the test \(MSE\) that we got using \(\lambda\) = 4. Finally, we refit our ridge regression model on the full data set, using the value of \(\lambda\) chosen by cross-validation, and examine the coefficient estimates.

> out <- glmnet(x, y, alpha = 0)

> predict(out, type = "coefficients", s = bestlam)[1:20,]

(Intercept) AtBat Hits HmRun

15.44383135 0.07715547 0.85911581 0.60103107

Runs RBI Walks Years

1.06369007 0.87936105 1.62444616 1.35254780

CAtBat CHits CHmRun CRuns

0.01134999 0.05746654 0.40680157 0.11456224

CRBI CWalks LeagueN DivisionW

0.12116504 0.05299202 22.09143189 -79.04032637

PutOuts Assists Errors NewLeagueN

0.16619903 0.02941950 -1.36092945 9.12487767

As expected, none of the coefficients are zero, ridge regression does not perform variable selection!

Using the Boston dataset, try determining the lambda that minimizes the \(MSE\) (store it in bestlam) using the cross-validation approach (store the cross-validation output in cv.out).

With the acquired \(\lambda\), determine the ridge regression predictions (store them in ridge.pred) and calculate the \(MSE\) (store it in ridge.mse).

Assume that:

- The

MASSandglmnetlibraries have been loaded - The

Bostondataset has been loaded and attached - The seed is set on 1.

- The variables

x,ycreated in exercise Ridge Regression 1 are already loaded - The variables

train,test,y.testandridge.modcreated in exercise Ridge Regression 4 are already loaded