We saw that ridge regression with a wise choice of \(\lambda\) can outperform least

squares as well as the null model on the Hitters data set. We now ask

whether the lasso can yield either a more accurate or a more interpretable

model than ridge regression. In order to fit a lasso model, we once again

use the glmnet() function; however, this time we use the argument alpha=1.

Other than that change, we proceed just as we did in fitting a ridge model.

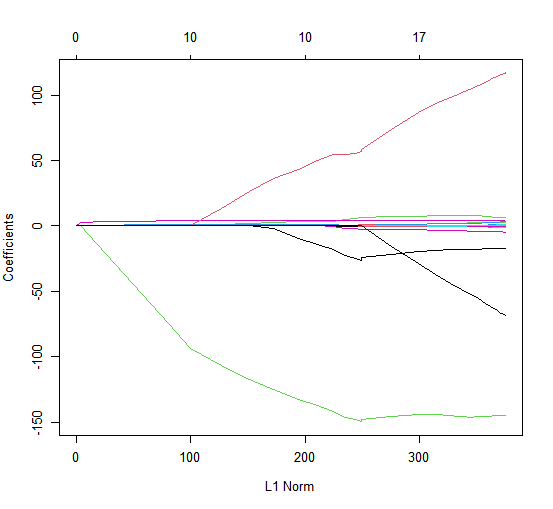

lasso.mod <- glmnet(x[train,], y[train], alpha = 1, lambda = grid)

plot(lasso.mod)

We can see from the coefficient plot that depending on the choice of tuning parameter, some of the coefficients will be exactly equal to zero. We now perform cross-validation and compute the associated test error.

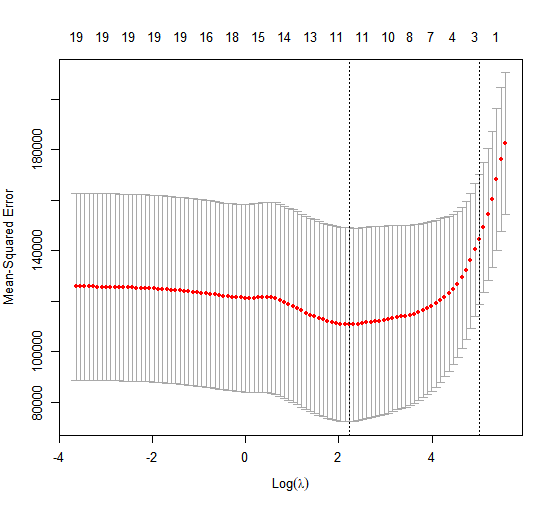

> set.seed(1)

> cv.out <- cv.glmnet(x[train,], y[train], alpha = 1)

> plot(cv.out)

> bestlam <- cv.out$lambda.min

> lasso.pred <- predict(lasso.mod, s = bestlam, newx = x[test,])

> mean((lasso.pred - y.test)^2)

[1] 143673.6

This is substantially lower than the test set \(MSE\) of the null model and of least squares, and very similar to the test \(MSE\) of ridge regression with \(\lambda\) chosen by cross-validation.

However, the lasso has a substantial advantage over ridge regression in that the resulting coefficient estimates are sparse. Here we see that 12 of the 19 coefficient estimates are exactly zero. So the lasso model with \(\lambda\) chosen by cross-validation contains only seven variables.

> out <- glmnet(x, y, alpha = 1, lambda = grid)

> lasso.coef <- predict(out, type = "coefficients", s = bestlam)[1:20,]

> lasso.coef

(Intercept) AtBat Hits HmRun

1.27479059 -0.05497143 2.18034583 0.00000000

Runs RBI Walks Years

0.00000000 0.00000000 2.29192406 -0.33806109

CAtBat CHits CHmRun CRuns

0.00000000 0.00000000 0.02825013 0.21628385

CRBI CWalks LeagueN DivisionW

0.41712537 0.00000000 20.28615023 -116.16755870

PutOuts Assists Errors NewLeagueN

0.23752385 0.00000000 -0.85629148 0.00000000

> lasso.coef[lasso.coef != 0]

(Intercept) AtBat Hits Walks

1.27479059 -0.05497143 2.18034583 2.29192406

Years CHmRun CRuns CRBI

-0.33806109 0.02825013 0.21628385 0.41712537

LeagueN DivisionW PutOuts Errors

20.28615023 -116.16755870 0.23752385 -0.85629148

Using the Boston dataset, try determining the lambda that minimizes the \(MSE\) (store it in bestlam) using the cross-validation approach (store the cross-validation output in cv.out).

With the acquired \(\lambda\), create a Lasso Regression model lasso.mod with bestlam as the lambda parameter, then determine the lasso regression predictions (store them in lasso.pred) and calculate the \(MSE\) (store it in lasso.mse).

Assume that:

- The

MASSandglmnetlibraries have been loaded - The

Bostondataset has been loaded and attached - The variables

x,ycreated in exercise Ridge Regression 1 are already loaded - The variables

train,testandy.testcreated in exercise Ridge Regression 4 are already loaded - The seed has been set on 1