Variable Importance in Random Forest

In this exercise, we will delve into the concept of variable importance

in the context of the random forest algorithm in R.

The randomForest, AUC and iml packages are required for this exercise.

We will use the data_sets.Rdata to illustrate the concept of variable importance.

Loading Required Packages and Data

if (!require("pacman")) install.packages("pacman"); require("pacman")

p_load(tidyverse, randomForest, iml)

Building the Random Forest Model

To be able to extract the variable importance,

a random forest model needs to be constructed with importance = TRUE.

rFmodel <- randomForest(

x = BasetableTRAIN,

y = yTRAIN,

ntree = 1000,

importance = TRUE

)

Understanding Variable Importance

Variable importance is a key aspect of a random forest model.

It allows us to understand which variables contribute the most to the model’s predictive power.

We can extract the variable importance from our model using the importance function.

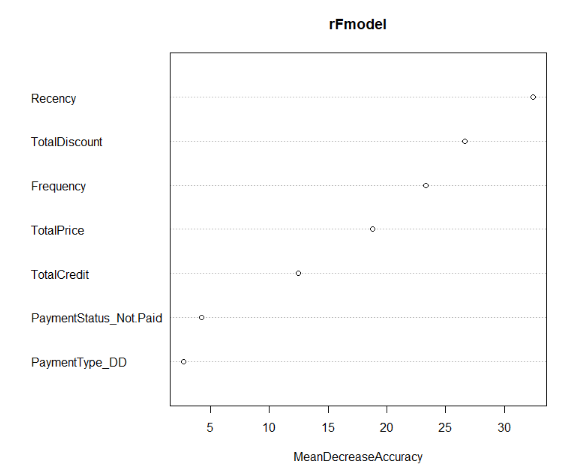

importance(rFmodel, type = 1)

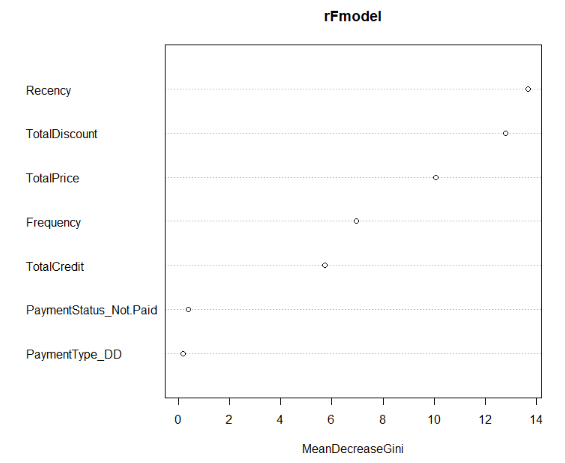

importance(rFmodel, type = 2)

importance(rFmodel, type = 1)

MeanDecreaseAccuracy

TotalDiscount 26.623587

TotalPrice 18.805011

TotalCredit 12.464571

PaymentType_DD 2.7294190

PaymentStatus_Not.Paid 4.2369690

Frequency 23.301393

Recency 32.408494

importance(rFmodel, type = 2)

MeanDecreaseGini

TotalDiscount 12.8097503

TotalPrice 10.0593459

TotalCredit 5.72686520

PaymentType_DD 0.17638050

PaymentStatus_Not.Paid 0.38232450

Frequency 6.94735730

Recency 13.6770525

A nice tabular view of the importances can be obtained by the following code block.

(impAcc <- importance(rFmodel, type = 1) %>%

as_tibble(., rownames = 'Features') %>%

arrange(desc(MeanDecreaseAccuracy)))

(impGini <- importance(rFmodel, type = 2) %>%

as_tibble(., rownames = 'Features') %>%

arrange(desc(MeanDecreaseGini)))

Features MeanDecreaseAccuracy

1 Recency 32.4

2 TotalDiscount 26.6

3 Frequency 23.3

4 TotalPrice 18.8

5 TotalCredit 12.5

6 PaymentStatus_Not.Paid 4.24

7 PaymentType_DD 2.73

Features MeanDecreaseGini

1 Recency 13.7

2 TotalDiscount 12.8

3 TotalPrice 10.1

4 Frequency 6.95

5 TotalCredit 5.73

6 PaymentStatus_Not.Paid 0.382

7 PaymentType_DD 0.176

Visualizing Variable Importance

Visualizing the variable importance can provide a more intuitive understanding. We can create a dot plot of the variable importance.

varImpPlot(rFmodel, type = 1)

varImpPlot(rFmodel, type = 2)

Using the iml Package

Also, the iml package can be used.

This is a more general interpretable machine learning package.

It allows you to calculate feature importance by several loss functions and for any model.

The FeatureImp function has several loss functions based on the metrics package library(help = "Metrics").

First, create a predictor object. We specify class 2 since we want to get our second factor (i.e. 1).

mod <- Predictor$new(

model = rFmodel,

data = BasetableTRAIN,

y = yTRAIN,

type = 'prob',

class = 2

)

Next, create a new object with loss function. We create the loss function with classification error (or 1 - accuracy). Since the model always calculates the increase in error, calculating the increase in classification error is the same as calculating the decrease in accuracy.

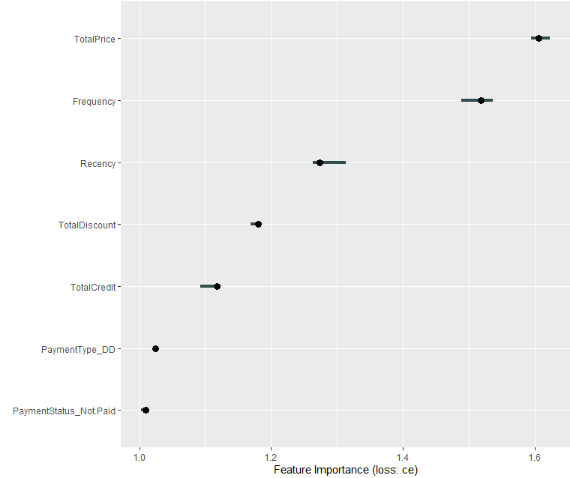

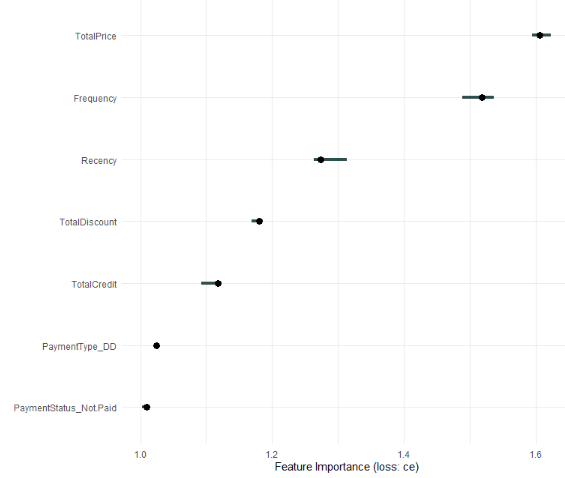

(imp <- FeatureImp$new(mod, loss = 'ce'))

Interpretation method: FeatureImp

error function: ce

Analysed predictor:

Prediction task: unknown

Analysed data:

Sampling from data.frame with 707 rows and 7 columns.

Head of results:

feature importance.05 importance importance.95 permutation.error

1 TotalPrice 1.594410 1.605590 1.622981 0.7312588

2 Frequency 1.488820 1.518634 1.536025 0.6916549

3 Recency 1.263975 1.273292 1.313043 0.5799151

4 TotalDiscount 1.168944 1.180124 1.185714 0.5374823

5 TotalCredit 1.093168 1.118012 1.122981 0.5091938

6 PaymentType_DD 1.022360 1.024845 1.024845 0.4667610

Confidence bands 5 % and 95 % are also reported.

The importance column is the median permutation importance over 5 repetitions runs.

By default, the ratio in model error is reported.

The difference in model can be seen by adding compare = 'difference'.

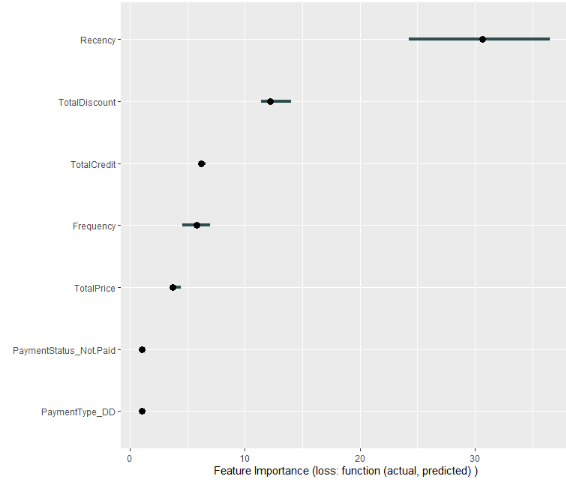

A plot can be made as well.

plot(imp)

This is a ggplot object, so you can play around with it.

plot(imp) + theme_minimal()

For another measure like AUC, create your own loss function.

imp <- FeatureImp$new(mod, loss = function(actual, predicted) 1 - Metrics::auc(actual, predicted))

plot(imp)

Exercise

Find the MeanDecreaseAccuracy for the variables in the model. Order the MeanDecreaseAccuracies from small to big and store them in impAcc. The other parameters of the random forest model remain the same. Do not use the iml package.

To download the Covid-19 data click: here1

Assume that:

- The randomForest library has been loaded.

- The

Covid-19data has been loaded.